The pandemic has changed the revenue drivers for skilled nursing providers.

Revenue recovery & diversification

Post-acute care, which nationally has tended to be less than 25% of patient days of care but has been the lifeblood of financial viability, has been hit hard — first, by a sharp decline in elective surgeries and overall declines in utilization across many types of care, as well as a strong preference for home-based rehabilitation.

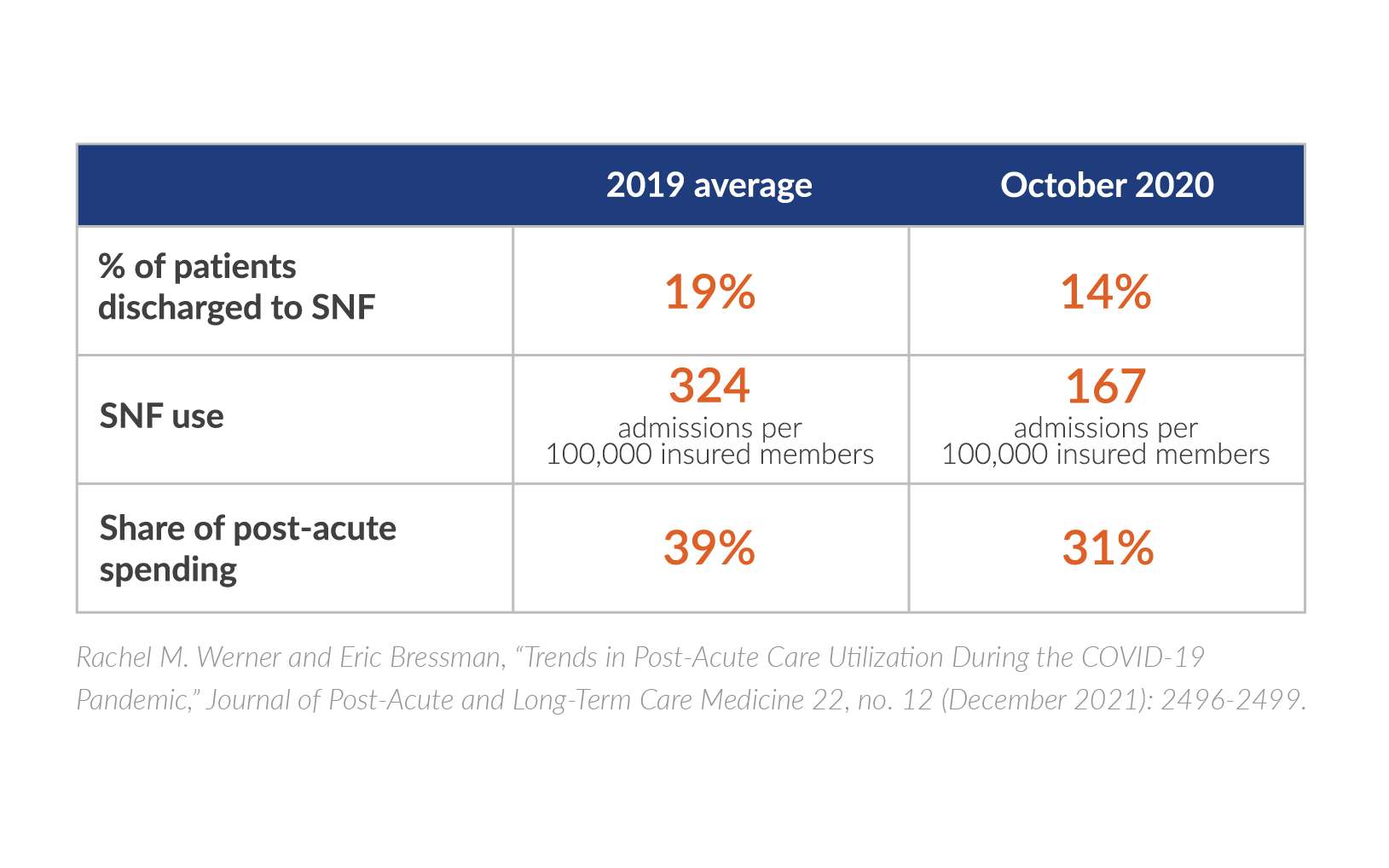

These trends drove a steep decline in post-acute care utilization. The percentage of patients discharged to SNFs from hospitals declined five percentage points from its 2019 average to just 14% in October 2020, according to a study of more than 70 million commercially insured individuals, including Medicare Advantage (MA) beneficiaries. Use of SNFs for post-acute care declined to 51% of the pre-pandemic rate, from an average of 324 admissions per 100,000 insured members to 167 admissions per 100,000. As a result, SNFs saw their share of post-acute spending drop eight percentage points. (See chart.) The study’s authors state that these trends point to “a fundamental shift in providing post-acute care at home, rather than in nursing homes.”

Will this shift to home last? The answer largely depends on whether lawmakers strengthen the home health benefit, which has shrunk over the course of the last decade. But the pandemic could represent an inflection point, given the imperative to reduce infection rates.

The Choose Home Care Act of 2021 proposes to supplement the traditional Medicare home health benefit with expanded services, including transportation, meals, home modifications, remote patient monitoring, telehealth services, and personal care services. Some industry leaders have expressed concern that the bill would limit options for Medicare beneficiaries, but others in the SNF community see advantages in creating incentives for more SNFs to offer at-home services.

Meanwhile, the number of Medicare Advantage plans offering home care as a supplemental benefit is on the rise, although managed care plans cap the benefit at a very low level (around 60 hours).

Whether you see home care as a complement or a competitor, all of these factors cast a specter of doubt on the long-term financial viability of the transactional, post-acute care side of the business.

New revenue streams for long-term care business

Given the decline in utilization of post-acute care, SNF owners and operators are understandably turning their attention to how to make the long-term care side of the house more attractive to residents and financially viable for the long haul.

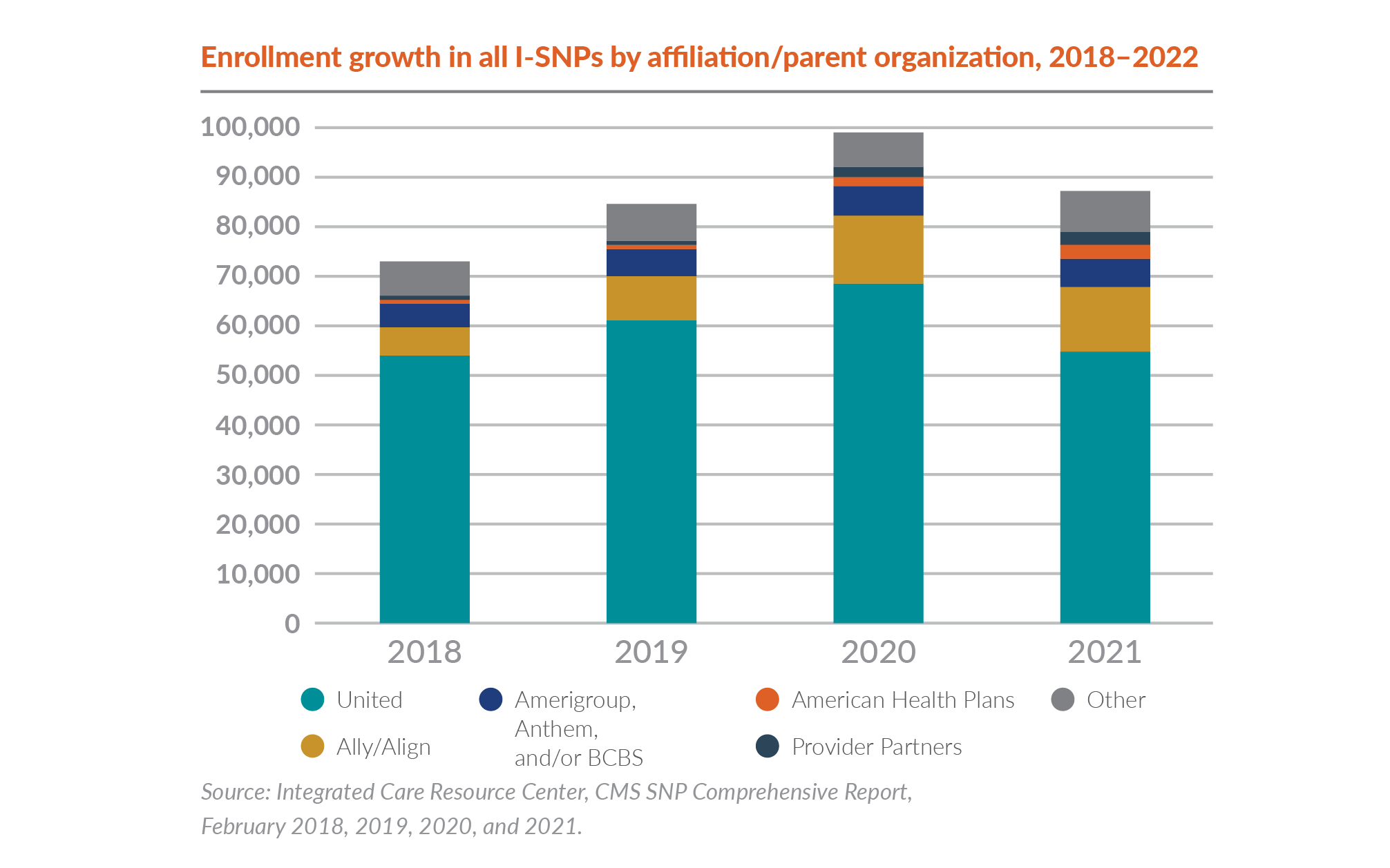

Population health strategies carry the potential for long-term care operators to create new revenue streams while improving residents’ quality of life. One of these options is the institutional special needs plan (I-SNP), a Medicare benefit for residents of long-term care institutions. Enrollment in I-SNPs saw strong growth in the years leading up to the pandemic. And while enrollment growth slipped in 2021, these plans remain one of the best vehicles for providers of long-term care to embrace first.

Nursing home owners and operators benefit from a new revenue stream associated with the I-SNP contract. In addition to a monthly fixed payment to help coordinate the care of the beneficiary, the nursing home also has opportunities to share in savings from managing the resident’s overall care costs, including hospitalization. Nursing homes can choose from a range of options that entail different levels of risk and reward. Some providers even establish their own I-SNPs.

Most importantly, the I-SNP will partner with the facility to strengthen clinical competencies that will help to avoid unnecessary hospitalizations and emergency department visits. This benefits residents and will also help facilities prepare for the continued growth of value-based contracts.

I-SNPs: A primer

What is an I-SNP?

A special needs plan (SNP) is a MA plan targeted to a specialized population. Institutional special needs plans (I-SNPs) target older, more frail residents who live in a long-term care setting. CMS requires each I-SNP to have a model of care, which spells out how the plan will take care of the beneficiary.

What does an I-SNP cover?

Typically, these all-in-one plans cover all traditional Medicare inpatient and outpatient services as well as prescription drugs. Each member is stratified into a risk level, which determines their individual care plan. In a SNP, certain encounters aren’t subject to the same medical necessity requirements as traditional Medicare, which means the beneficiary can receive more frequent visits. I-SNPs are also permitted to provide additional benefits that aren’t included as part of traditional Medicare.

What are the advantages of an I-SNP?

Residents gain better care coordination provided to them by the place they have chosen as their home, as well as customized benefits that are tailored to nursing home residents. Providers should take time to understand the range of risks and opportunities entailed by these programs. The I-SNP and the nursing home both benefit when the total cost of the resident care is managed effectively and the clinical outcomes are strong.

Nursing home owners and operators benefit from a new revenue stream associated with the I-SNP contract. In addition to a monthly fixed payment to help coordinate the care of the beneficiary, the nursing home also has opportunities to share in savings from managing the resident’s overall care costs, including hospitalization. Nursing homes can choose from a range of options that entail different levels of risk and reward. Some providers even establish their own I-SNPs.

Most importantly, the I-SNP will partner with the facility to strengthen clinical competencies that will help to avoid unnecessary hospitalizations and emergency department visits. This benefits residents and will also help facilities prepare for the continued growth of value-based contracts

Skilled nursing providers also have opportunities to build on the momentum to provide more healthcare services in the home. Two population health programs create opportunities to provide nursing home services “without walls.”

An institutional equivalent SNP (IESNP) is designed for residents who live in their homes or in assisted living communities but require an institutional level of care (LOC). A determination of institutional LOC is based on the use of the same state assessment tool that’s used for individuals residing in an institution. The assessment must be administered by an independent, impartial party with the professional knowledge to identify the institutional LOC needs. IESNPs may be appropriate for life plan communities and assisted living providers. In addition, skilled nursing providers that have experience with I-SNP are considering how to leverage that model into other settings with IESNPs.

Program of All-inclusive Care for the Elderly (PACE®) is an integrated care program for nursing home-eligible residents that have both Medicare and Medicaid benefits and who can live safely at home. The PACE model of care has been around since the 1970s, but the high cost of building and regulating PACE centers has been a limiting factor in their growth. Success with PACE is greatly correlated to state Medicaid payment rates. There are some compelling reasons why senior care and living providers should weigh the benefits of a PACE program. During the pandemic, the model proved a successful alternative to skilled nursing care, with PACE providers pivoting almost overnight to home-based services. In response to pandemic success, and increased funding for home and community-based services, many states are looking to expand PACE programs.

Optimizing existing revenue streams

Long-term care providers also must find ways to optimize their existing revenue streams.

The most significant change in Medicare payment methodology in 20 years, the Patient-Driven Payment Model (PDPM) was initially viewed by the industry with some trepidation. However, PDPM so far has been overwhelmingly positive for skilled nursing providers, who have seen average increases of 5 to 10% over previous reimbursement rates.

The COVID-19 pandemic, which hit only five months after PDPM was implemented, has been a significant factor in driving higher reimbursement rates, as PDPM rates are higher for patients with greater clinical needs. Since PDPM was designed to be budget-neutral, skilled nursing providers should prepare themselves for a possible reckoning in fiscal year 2023.

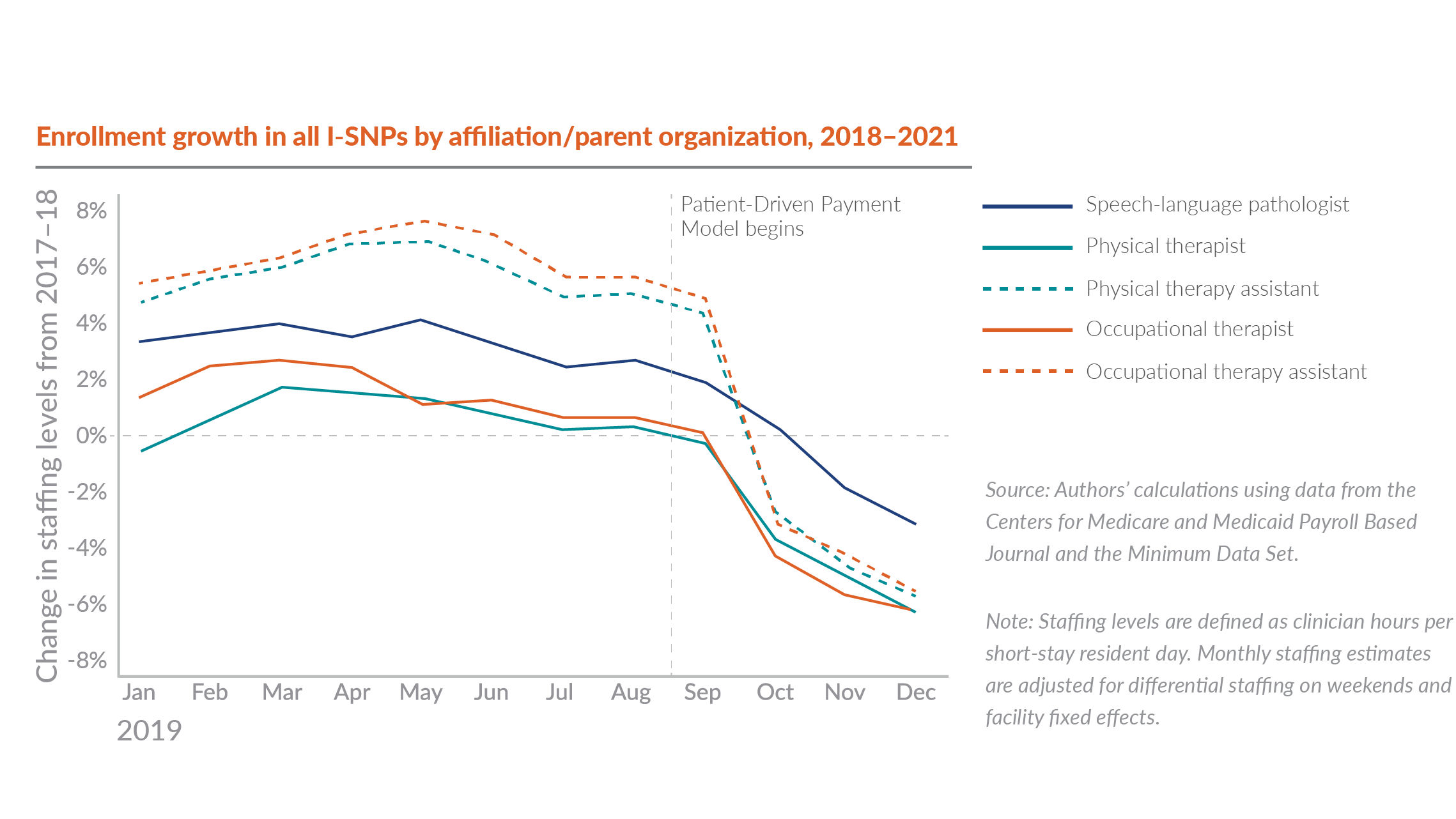

Providers also are seeing significantly reduced therapy services. Total therapy minutes per patient-day declined sharply following PDPM implementation, followed by more gradual declines over the next six months for a total decline of 14.7% by the end of March 2020. Physical and occupational therapy disciplines experienced roughly parallel declines. (See chart below.)

SNFs must engage in ongoing monitoring to ensure these therapy reductions don’t have negative implications for patients. However, the reduced staffing costs have been welcome at a time when staff is in short supply and nearly every other expense has escalated significantly.

To achieve optimal PDPM rates, SNFs should:

- Focus on accurate capture and coding of each patient’s entire clinical diagnoses. Take the time to revisit training and processes that were put in place when PDPM was first implemented. Given today’s staffing shortage, overwhelmed MDS nurses might overlook some of a patient’s clinical diagnoses at admission. For example, speech language pathology requires close coordination between the dietary and speech departments, and lack of communication between those departments can hurt reimbursement.

- Monitor your region’s average PDPM rate. If your organization’s rates differ significantly from those averages, investigate whether there are opportunities to capture more detailed information to increase those rates.

- Review any Medicare Advantage contracts. Some MA plans have adopted Medicare’s reimbursement methodology, so optimizing the PDPM rate can have a beneficial effect on multiple revenue streams.

The past two decades have seen a steady shift from traditional Medicare to MA. In 2021, Medicare Advantage plans had more than 26 million enrollees — about 42% of the total Medicare population and 46% of total Medicare spending. On the current trajectory, MA enrollment will be higher than the traditional Medicare rolls by 2030.

Perhaps most astonishing is the fact that the average Medicare beneficiary in 2021 could choose among 33 MA plans, which means that providers are keeping track of a staggering array of claim criteria, reimbursement rates, submission processes, and billing time frames.

Optimizing managed care reimbursement from MA or other commercial plans comes down to three things:

- Cost containment. Make sure you’re managing your ancillary costs for the managed care individual. Therapy is a huge cost area for both Medicare and managed care. Each plan has different requirements for therapy delivery. Whereas one plan might require 80 minutes of therapy per week, another requires 100 minutes. With the conversion to PDPM, many administrators aren’t placing the same level of priority on tracking therapy minutes, but keep in mind that oversights can lead to denied claims and underpayments.

- Understanding your organization’s financial performance. Providers need to clearly understand each plan’s requirements and how their actual costs (routine and capital costs from Medicare cost report plus ancillary costs, such as therapy, pharmacy, lab, and X-ray) compare to the managed care rates. Many providers will find that the managed care rates are lower than their actual costs. Armed with this information, they can make informed decisions about renegotiating or terminating these unprofitable plans.

- Annual contract renegotiations. While it can be all too easy for overwhelmed administrators to let contract renewal periods slide, a provider’s long-term financial health depends on regular evaluation of contracted rates. Come to the negotiating table armed with research on market rates and your cost to provide services under these contracts.

Pandemic financial performance: How bad was it?

Overall financial performance of the SNF industry is regularly evaluated by various stakeholders, primarily using public data provided on Medicare cost reports. These reports are filed five months after a provider’s year-end and aren’t available for public analysis until several months after that.

The Medicare Payment Advisory Commission (MedPAC) reported findings in March of 2022 that reflected an industry “all payer” net margin. Aggregate Medicare margins also increased from 11.9% in 2019 to 16.5% in 2020. These findings informed its recommendation to reduce SNF payment rates in fiscal year 2023.

While this margin growth may seem hard to believe, keep in mind that the financial impacts of the pandemic have unfolded in waves. For example, census drops were most dramatic late in 2020, whereas labor costs rose steeply throughout 2021. MedPAC acknowledged that the improvement in margin was largely due to both federal and state public health emergency funding.

Also consider that individual providers experienced the pandemic’s financial impacts at varying rates and time periods that may not align to the overall trends. There has also been significant variation in the timing and amount of federal relief funds, state Medicaid, and other assistance.

We expect that 2021 cost report data will reflect significantly lower industry all payer and Medicare margins, reflective of continued slow census recovery and the rising cost of labor. Individual facility results will continue to vary widely, particularly for entities that have been able to file for payroll protection program loans and employee retention credits.

How does my organization compare?

In prior reports, we have provided extensive historical benchmarks on revenue drivers and operating costs. Given the impact of the pandemic, benchmarking current key performance indicators can be far more informative than looking back at historical data. While it can be a challenge to find current benchmarks, two reliable sources of benchmarking data for SNFs include:

- The National Healthcare Safety Network (NHSN) database, which was expanded during the pandemic to include the reporting of weekly census information.

- Payroll-based journal data published by CMS, which provides insight on competitor staffing levels.

As you benchmark your financial performance against peers in your market and seek ways to optimize current revenue streams, be sure to learn about the risks and opportunities of population health strategies with the potential to create new sources of revenue while improving residents’ quality of life.

Reimagining the future of senior care

Demand for senior care services will continue to build, even if the pace of recovery remains uncertain. Organizations that remain agile will be prepared to respond to the long-term demographic boom of seniors, while those that cling to status quo will be left behind. Now’s the time to future-proof your senior care organization with strategies that balance the needs of today with the long-term care landscape of tomorrow.

Let’s work together to reimagine the future of senior care and find ways to thrive amid uncertainty